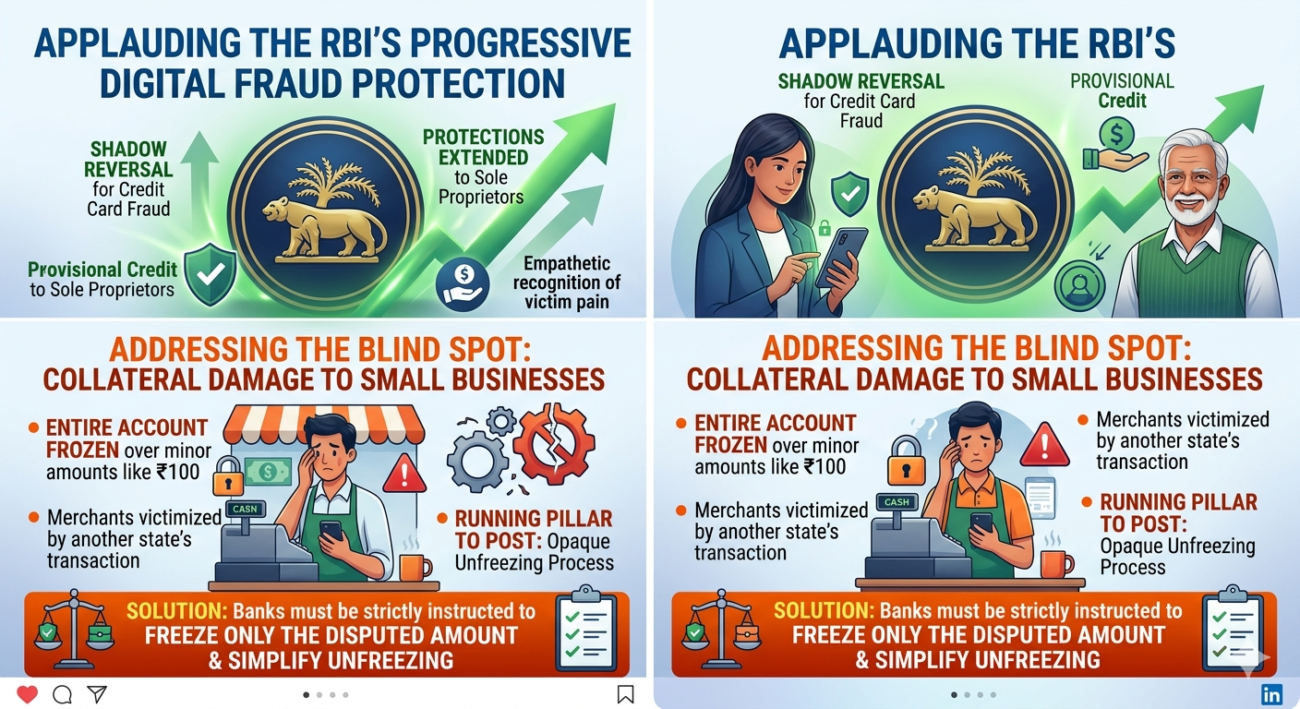

The Reserve Bank of India (RBI) deserves immense credit for its newly finalized digital banking fraud protection guidelines. By introducing the shadow reversal mechanism for credit card fraud and explicitly extending small-value fraud protections to sole proprietors, the central bank has shown a deep, empathetic understanding of the pain points that ordinary citizens and small business owners face daily.

Steps like forcing swift provisional credit and reducing alert thresholds are exactly what a progressive digital economy needs to foster trust. 💡

However, there remains a massive, unaddressed blind spot: the collateral damage on unwitting small businesses.

Currently, when cybercriminals funnel stolen money through the digital ecosystem, innocent merchants and small businesses who accept these funds for legitimate goods or services are being severely penalized.

The reality on the ground is alarming:

🛑 disproportionate Actions: Entire bank accounts of small business owners are being frozen over meager, incidental amounts—sometimes as low as ₹100 of “tainted” money.

🛑 Jurisdictional Nightmare: If the transaction or cyber complaint originates from another state, the business owner is forced to run from pillar to post, coordinating across state borders just to prove their innocence.

🛑 Working Capital Paralyzed: A blanket freeze over a minor disputed amount completely halts a small business’s daily operations, destroying their livelihood over a crime they had zero part in.

The Solution Needed: While we protect the victims of scams, we must not victimize innocent participants in the commerce chain.

1️⃣ Lien/Freeze Only the Disputed Amount: Banks must be strictly instructed to freeze or put a lien only on the specific disputed amount, rather than locking the entire account.

2️⃣ Simplify the Unfreezing Process: We desperately need a centralized, digital, and streamlined standard operating procedure (SOP) to unfreeze accounts swiftly once the merchant demonstrates a legitimate business transaction.

Kudos to the RBI for taking giant strides toward customer protection. Let’s hope the next phase of regulations brings much-needed relief to the small business ecosystem that keeps India running.

What are your thoughts on how we can better balance fraud prevention with merchant protection? Let’s discuss in the comments. 👇